As a Brisbane‑based financial advice practice in Fortitude Valley we are already speaking with clients across the inner city – including New Farm, Teneriffe, Newstead and the wider south‑east Queensland region – about what the 2026‑27 Federal Budget really means for their long‑term plans. The key proposals around capital gains tax (CGT), negative gearing and discretionary (family) trusts will be especially relevant for property investors, business owners and families building wealth outside superannuation, but most changes are still some time away and do not require rushed decisions today.

The 2026‑27 Federal Budget included several significant tax proposals targeting capital gains tax (CGT), negative gearing and discretionary (family) trusts. These measures are aimed at how wealth is built and taxed outside superannuation, particularly for investors and business owners.

Most of the major changes are not due to commence until at least 1 July 2027, and they are still proposals rather than law. Importantly, none of the headline measures change the existing rules for superannuation in either accumulation or pension phase, so current super strategies remain on the same footing for now.

Key message

For most investors and business owners, these proposals may influence how future investments are structured and how certain strategies are used, but there is no need to rush into decisions today. The details will likely evolve as legislation is drafted and debated. Our focus is to understand how the final rules apply to you personally and then integrate them thoughtfully into your long‑term plan rather than reacting to headlines.

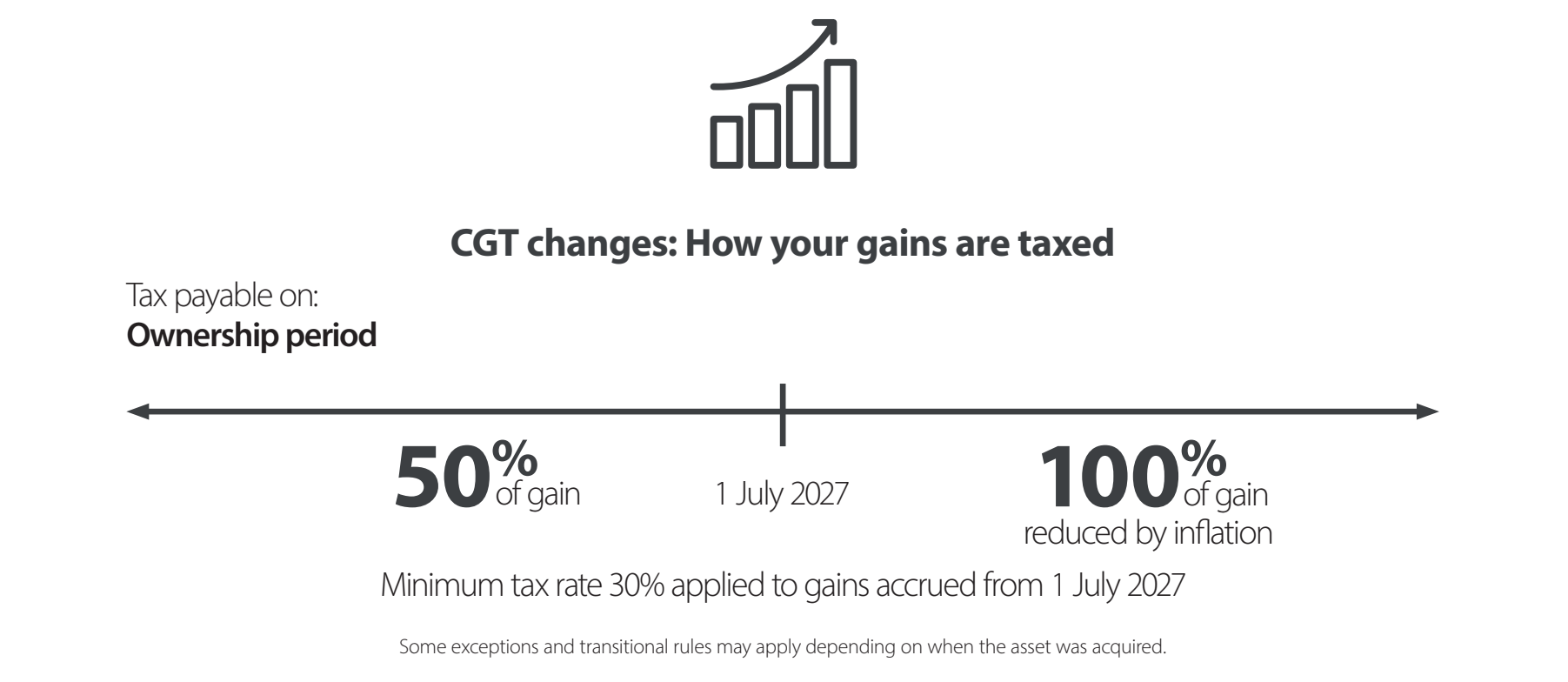

1. Capital gains tax: changes to the discount and a new minimum rate

Under current rules, individuals and many trusts that hold a growth asset (such as shares or property) for more than 12 months can generally reduce the taxable capital gain by 50%. The Budget proposes to move away from this simple 50% CGT discount for gains that accrue from 1 July 2027, and to introduce a new minimum tax outcome for many taxpayers.

Although the final details will depend on the legislation, the direction of travel is clear: larger gains held outside super are more likely to be taxed at higher effective rates than they are today. The tax‑free status of pension‑phase super and the concessional CGT settings inside super are not being changed by these measures, which leaves superannuation as a relatively attractive environment for long‑term investing.

For you, this may affect:

-

How we think about holding assets personally, in a trust or inside super.

-

The timing of selling long‑held growth assets, particularly where significant gains have built up.

-

The trade‑off between flexibility (for example, holding assets in your own name or a trust) and long‑term tax efficiency.

Any decision to sell or restructure investments purely because of the proposed CGT changes should be made carefully and only once we have clear law and tailored advice. In some cases, the cost of triggering CGT early could outweigh the benefit of any future tax changes.

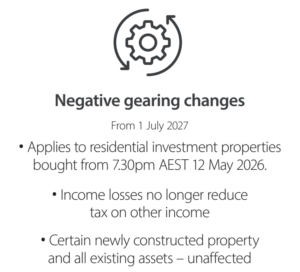

2. Negative gearing: quarantining future property losses

Negative gearing occurs when the costs of holding an investment (such as interest, repairs and other expenses on a rental property) are higher than the income it produces, and the resulting loss is used to reduce other taxable income like wages.

The Government has announced changes that would apply to new residential property investments acquired after Budget night. From 1 July 2027, rental losses on these new properties would generally be “quarantined”. Instead of offsetting salary or other income, those losses could only be used to offset future rental profits from that property (or potentially other rental income, depending on the final rules).

For existing negatively geared properties, the current rules are expected to continue, so this proposal is largely about reshaping the incentives for future property investors rather than retrospective changes to existing holdings. For clients considering buying investment property over the next few years, this may:

-

Reduce the after‑tax benefit of highly leveraged property strategies.

-

Increase the importance of the underlying investment case (rental demand, growth prospects, diversification) rather than relying on tax benefits.

-

Change the relative appeal of property versus other investment options, especially if the CGT and trust changes are also relevant.

Again, this is a reason to carefully model future purchases, not to panic or liquidate existing assets.

3. Discretionary trusts: a 30% minimum tax on most distributions

Discretionary (family) trusts are widely used by families and business owners to hold investments, operate businesses and manage intergenerational wealth. At present, trustees can often distribute income to beneficiaries on lower marginal tax rates, which can result in lower overall tax bills.

The Budget proposes to introduce a 30% minimum tax on most distributions from discretionary trusts from 1 July 2028. Some types of trusts (for example, possibly certain charitable or special‑purpose trusts) and some categories of income may be carved out, and limited rollover relief is proposed from 1 July 2027 to help restructure out of certain arrangements.

In practice, this could mean:

-

Less benefit from distributing investment or business income to adult family members on low incomes purely for tax reasons.

-

A shift in the relative attractiveness of trusts versus companies or direct ownership in some situations.

-

A need to review existing trust‑based strategies for managing business profits, investment income and succession planning.

Because trusts can hold valuable assets (such as operating businesses, farms, investment portfolios or properties), any structural change must be approached carefully. Transfers can trigger CGT, stamp duty and other costs, and there are legal and estate‑planning issues to consider. The proposed rollover relief may help in some cases, but it is unlikely to be a “one size fits all” solution.

Other key measures to be aware of

While CGT, negative gearing and trusts are the three big structural tax themes, the Budget also includes several other measures that may be relevant:

-

Electric vehicles and fringe benefits tax (FBT) – The current FBT exemption for many electric vehicles is proposed to be wound back progressively from 1 April 2027. This will matter most to employees and business owners using salary packaging or novated leases for EVs, as the after‑tax cost of running a vehicle may rise over time.

-

Small business instant asset write‑off – The Budget proposes to make the $20,000 instant asset write‑off a permanent feature for eligible small businesses with turnover up to $10 million. This can simplify decisions about replacing or upgrading equipment, although it remains a timing benefit rather than “free money”.

-

Personal tax cuts – Previously announced personal income tax changes, including reductions to some lower marginal tax rates from 1 July 2026 and 1 July 2027, are confirmed. These changes deliver modest ongoing tax relief, putting a little more in the pocket of many workers and potentially supporting savings capacity.

Crucially, none of these measures alter the core superannuation rules in either accumulation or pension phase. The existing contribution caps, tax rates within super and tax‑free status of many retirement income streams remain the same under this Budget.

What does this mean for you?

Taken together, the proposed CGT, negative gearing and discretionary trust changes point towards a tax system that is less generous to some traditional wealth‑building strategies outside super, particularly for higher‑income households and those using more complex structures. At the same time, the relative attractiveness of superannuation’s existing tax concessions is reinforced.

For you, this may mean:

-

We place even more emphasis on using superannuation effectively, where appropriate for your life stage and access needs.

-

We scrutinise the case for new negatively geared property purchases more carefully, factoring in quarantined losses.

-

We review any trust‑based strategies well before the proposed start dates, to avoid last‑minute decisions and to make good use of any transitional rules.

For now, there is no need to make immediate changes purely in response to the Budget. Over the next 12–24 months, we will:

-

Track the progress of these measures as draft legislation is released and debated.

-

Model the impact of any final rules on your structures, investments and cashflow.

-

Discuss any recommended adjustments with you at your review meetings, prioritising those clients with property portfolios, family trusts or substantial non‑super investment holdings.

If you live or work in Brisbane – particularly in New Farm, Fortitude Valley, Teneriffe, Newstead or nearby suburbs – and would like tailored financial advice on how the Federal Budget proposals might affect your investments, property strategy or family trust, we can help. We work with clients across south‑east Queensland to build and protect wealth through considered, long‑term planning rather than reacting to short‑term Budget headlines. Get in touch to arrange a meeting in our Fortitude Valley office or via video.

Frequently asked questions

Do I need to change my investment strategy because of the Federal Budget 2026‑27?

For most people, there is no need to rush into changes. The major CGT, negative gearing and discretionary trust measures are still proposals and mostly start from 1 July 2027 or later. It is better to wait for final legislation and get personal advice.

How can a financial adviser in Brisbane help me with the Budget changes?

A local Brisbane financial adviser can model how the proposed rules might affect your property portfolio, superannuation, investment structures and cashflow, and then recommend practical steps that align with your goals and timeframes.

Do the Budget changes affect my superannuation?

None of the major Budget measures change the core rules for superannuation in either accumulation or pension phase. Your existing super strategy is not directly impacted, but the relative attractiveness of investing through super versus outside super may strengthen over time.